Monetary Realism… Is There No Alternative?

A Q&A with the artist Austin Houldsworth, who decided to make it his project to reimagine that which burdens so many creatives: money.

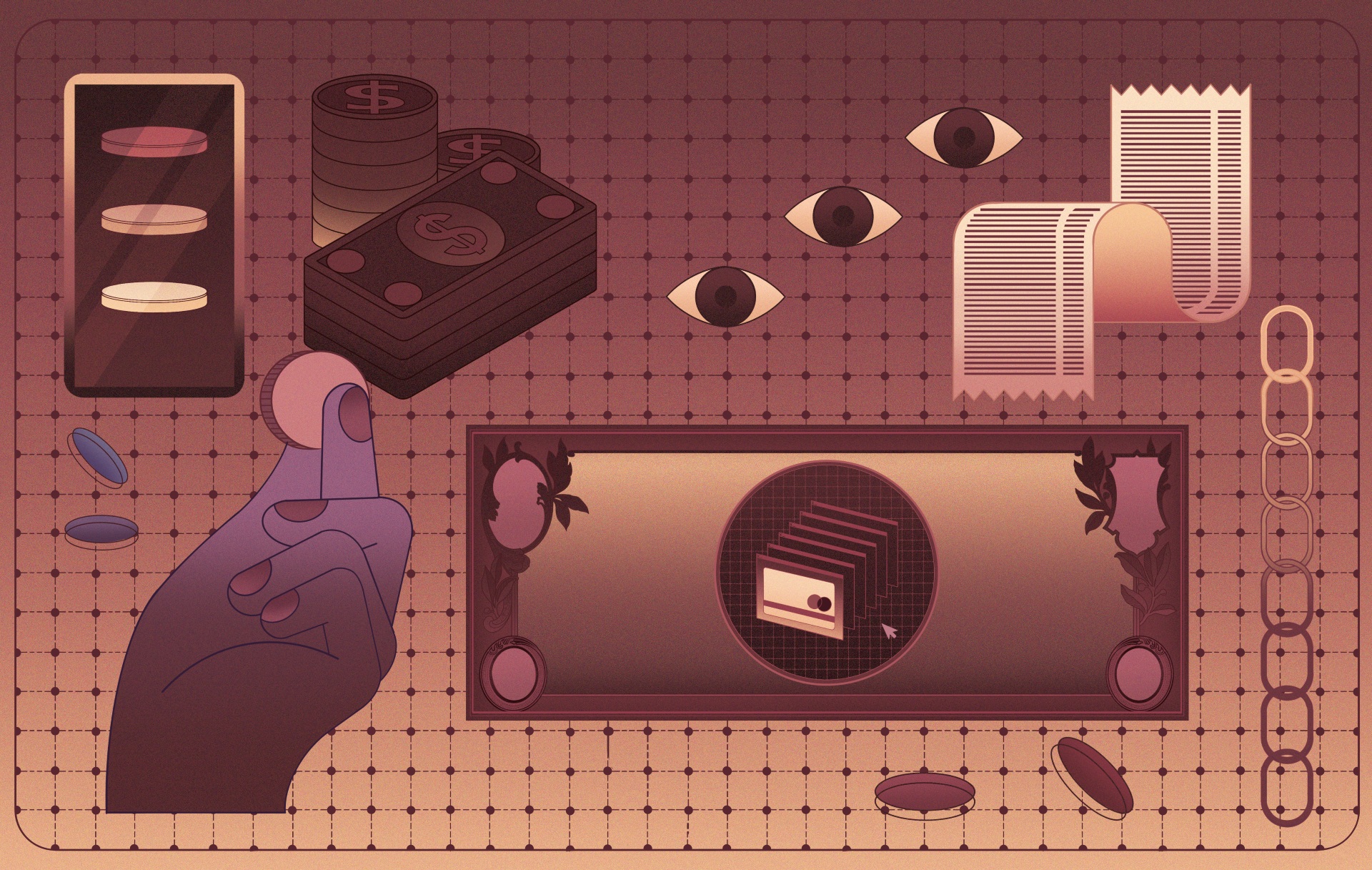

As digital payments take over, cash is disappearing – but should we think twice? From privacy concerns to power dynamics, the push toward a cashless society raises questions about control, choice, and trust.

Illustration: Sophia Prieto

Now that there are taxi services the likes of Uber, Brett Scott asks, should we get rid of bicycles? Or because there are elevators, should we stop building stairs? “Stairs suck! Until your elevator breaks down,” says the monetary anthropologist and author of Cloudmoney: Cash, Cards, Crypto, and the War for Our Wallets. To the same end, while there are good arguments for the digital payment systems that increasingly dominate our experience as consumers, “I have yet to hear a good argument for getting rid of cash,” Scott says.

Yet while the volume of notes and coins in the world is actually on the increase – thanks to a growing informal economy, low interest rates, and a broad, postcrash distrust of financial institutions, all of which is encouraging the hoarding of cash – the general impression may be that cash is on the way out. There are many predictions to the tune of ‘within a decade only one in seven payments will be made using cash’.

Broaden your horizons with a Futures Membership. Stay updated on key trends and developments through receiving quarterly issues of FARSIGHT, live Futures Seminars with futurists, training, and discounts on our courses.

become a futures memberThough culture and local conditions influence the acceptance of a ‘cashless society’– Germany, for instance, is a highly modern country yet has payment card usage around 30% – this is often mistakenly equated with progress. Who needs all that grubby, bulky paper stuff in a streamlined world of global, instantaneous, contactless transactions by app?

Sweden is the poster child for the digital transaction, where just 10% of payments are made using cash – down from 39% a decade ago. The same shift is afoot in South Korea. Last year its central bank started to phase out coins. In China, payment by smartphone is the norm, especially among the young, urban population. More than half the population there uses cashless payments, typically via apps like WeChat and AliPay.

Guillaume Lepecq, chair of the campaign group Cash Essentials, argues that the benefits of a cashless society are often overstated. While proponents claim it reduces crime, increases tax revenue, enhances security, and boosts economic growth, these points are debatable and frequently outweighed by opposing arguments.

Safer? Giant financial institutions the likes of JP Morgan, UniCredit, and Visa have all experienced serious systems crashes or malicious hacks. More convenient? That’s Marxist philosopher Antonio Gramsci’s idea of hegemony in action: the powerful condition the cultural environment until their interests appear natural and inevitable to the public. Consider self-service checkouts in supermarkets. They were also presented as a convenience for customers. When customers use this ‘convenience’, it’s given as evidence for their preference. Then checkouts manned by real people start to disappear.

“[Likewise], we need to challenge the narrative of a single digital future for money and argue that cash has unique attributes,” Lepecq says. “It’s financially and socially inclusive – cash doesn’t discriminate and doesn’t require digital literacy. And it’s economically and socially resilient. Cash is stabilising. When the system crashes, or there’s a crisis – as with Covid, with Y2K, or when a natural disaster is predicted – people turn to cash. And we certainly live in uncertain times now.”

Of course, Lepecq adds, the benefits lost in eliminating cash would be accompanied by actual dangers. A state doesn’t have to be authoritarian to want the capability to monitor every transaction its populace makes, or to see the anonymity of cash transactions as indicative of illegal activity. “Eliminating cash is a means of control,” as Lepecq puts it. “The threat to cash is not just about the rise of tech. It’s about who controls that tech.”

“Our behaviour on social media suggests people are increasingly willing to give up their data,” says Alan Goode, former HSBC executive and head of finance research at Goode Intelligence. “There’s a growing push towards ’naked’ biometric payment systems, like face and palm recognition. While we need to protect citizens, it seems only a vocal minority is thumbing through 1984 for warnings.”

According to Brett Scott, this debate goes far beyond convenience versus surveillance: it’s about the power dynamics shaping the entire monetary system. We are shifting from a public-private hybrid model – where public central banks issue cash and private banks issue digital units backed by cash or the promise to provide it – to a system that is essentially private.

He argues that while cash advocates are wary of central banks considering their own digital currencies – seeing it as yet another step away from cash by those meant to protect it – commercial banks and major fintech companies, like credit card firms and mobile payment apps, aren’t pleased with the idea either. With a central bank digital currency ostensibly more trustworthy and secure, commercial banks would also lose their dominance of the digital system and the money they earn from it.

The current imbalance in this public/private dynamic also leaves the private sphere free to dominate the conversation about cash. It can push the idea that a cashless future is to the consumer’s benefit when the real benefit is to banks’ bottom line. This explains their readiness to reduce staff numbers by closing branches and removing ATMs. Private banks can promote the notion that to oppose the transition is in some sense Luddite. Central banks, in contrast, are legally limited in promoting their ‘product’, cash.

“Central banks tell you it’s not their job to promote cash, that they’re agnostic, that they will continue to issue cash as long as demand is there. It’s a valid approach so long as cash is dominant,” says Lepecq. “But that’s not the case now, and the conversation is entirely asymmetric.”

Scott agrees that if cash was promoted by central banks, it would bring a big change in public perception regarding the cashless society. He adds, by way of example, that it was the private sphere which, over the pandemic, pushed the entirely bogus but widely accepted idea that cash is literally ‘dirty’. “Most people only interact with the digital economy at a very surface level so it’s very easy to promote things that are faster or ‘more efficient’ as ‘freeing up time in your life for other things’. Ask people if they want to use digital payments and most say yes. Ask them if they want cash taken away and typically they’ll say no. They want both, a choice.

Explore the world of tomorrow with handpicked articles by signing up to our monthly newsletter.

sign up here“It’s fintech, vendors, and the retail industry pushing people away from the choice. I think there’s a feeling of powerlessness surrounding this topic or an uncertainty about how to be activist against it,” he adds. “And that leaves many people just accepting it.”

Or, indeed, ending up with the opinion that to oppose a cashless future is in some way to fall foul of conspiracy theorising around Big Tech, Big Banking, Big State, and so on. That the debate is ideological, Scott contends, is suggested by the changing face of those who oppose this supposed progressive march into a cashless future.

Since the Covid era, right-wing groups have largely taken over the anti-tech, anti-corporate narrative. “They offer less of an analysis of the systemic problems of capitalism and more of a blame on small groups of ‘evil’ people – it’s all Bill Gates!” Scott laughs. Meanwhile, the left-wing has backed away from any corporate critique of the kind that was once natural to it for fear of being considered conspiratorial. “The pro-cash camp particularly should be part of left-wing thinking because it’s essentially about anti-privatisation,” he suggests.

The effect of the anti-cash sentiment also has a personal effect that these ideological abstractions don’t capture. “I don’t mind using digital payments,” says Scott, “but what really bothers me is this bullshit narrative pushed by the fintech industry that there is something shameful about using cash.”

The embarrassment or awkwardness experienced when pulling out cash to pay for a coffee, only to be met with the sour, disapproving expression of a twentysomething barista, stems from what Scott calls corporate gentrification and the cultural dominance of the international middle class. The use of cash even carries class divide connotations that see, for example, the hospitality business happy for its staff to take tips in cash, but which won’t take payment in cash itself.

“It’s a cultural process that spreads mimetically through the population,” reckons Scott. “We didn’t have this idea that cash was shameful 10 years ago. The idea is illusory but it’s hard to convince people of that without a counter movement to re-establish pride in the use of cash.”

Illusions are playing out in the bigger picture too. Scott argues that the cash debate is another example of the ‘progressive narrative’ dominant in contemporary culture: the idea that the only real progress is towards ever more speed and scale, and that this is only ever to the population’s advantage. “The idea that progress can be more human, or more local, isn’t one you hear coming out of megacorporations,” he notes. He sees the same thinking playing out with the advance of AI. First, it’s wondrous and convenient; next, we must use it or be left behind and marginalised.

“Getting people to see through this narrative is very important,” Scott argues. “We can have technological change, but we don’t need to fetishise it. And we have to keep the balance of power.”

“I’m often called a contrarian or a dinosaur because most people haven’t taken the time to think through the issues surrounding cashlessness,” agrees Lepecq. “The challenge is persuading them to do so.”

But perhaps the tide is already turning. Lepecq points out that businesses that once operated solely on card payments, such as Uber, are now looking to reintroduce cash payments. Recently, several US states and cities, as well as many European countries – France and Spain among them – have made it mandatory for businesses to accept cash. Brussels is also drafting EU-wide legislation to enforce this requirement.

There’s also the question of whether trust in the financial infrastructure will erode once cash disappears. “Remove the cash infrastructure and trust in the digital units collapses, because you can no longer redeem those units,” Scott says. “So while the narrative may say that cash will disappear, I don’t think so.”

Lepecq is less assured. “There’s still a bumpy road ahead for cash,” he says, noting that moves to phase out high denomination notes in many countries might well be read as a first step in priming the public for the phasing out of lower denomination ones too. Yet he offers another reason why he believes cash will likely win through in the end. Much as some banks were once described as ‘too big to fail’ – because government would have to bail them out to save the economy – soon the same phrase might be applied to cash.

“Cash has societal, political, historical, and emotional value,” Lepecq says. “It’s been called the most important system of trust ever devised. Take it away and something like it always comes up to take its place, as we see in prison cultures. Some institutions may have a vested interest in getting rid of the construct of cash, but the fact is that if it disappeared, we’d only have to invent it again.”

Get FARSIGHT in print.